Anúncios

Cost of Living Crisis Overview

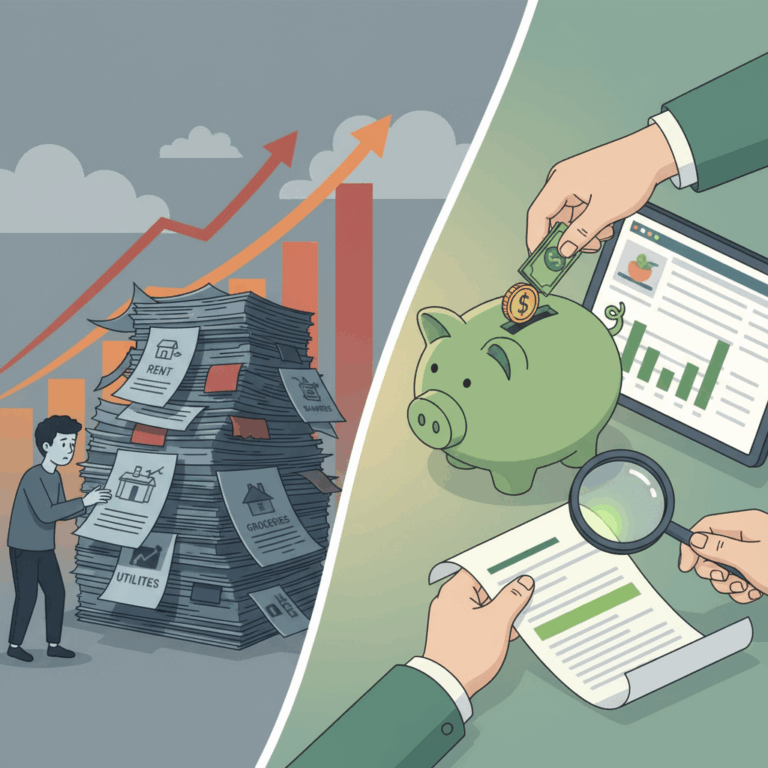

The cost of living crisis is driven by rising expenses for essential goods and services such as housing, food, energy, healthcare, and education. These price increases are outpacing wage growth, creating financial strain for many families.

Households face difficult choices as their purchasing power declines, with many struggling to cover basic needs despite nominal income gains. The persistent inflation challenges continue to affect everyday life deeply.

Anúncios

This overview sheds light on the key drivers of the crisis and its consequences on household finances, highlighting the need for awareness and adaptation strategies in these trying times.

Rising Expenses in Essential Goods and Services

Essential goods such as food have seen price increases of around 25% since 2021, while rents have climbed nearly 27%, severely impacting households’ budgets. Energy and healthcare costs also contribute significantly to the rising expenses.

Anúncios

The steady increase in prices comes despite some inflation easing recently, maintaining heightened costs that challenge families to meet their basic needs without advancing income levels.

These inflationary pressures mean that many people are forced to prioritize spending on essentials, often cutting back on non-essential items to survive financially in this environment.

Impact of Inflation on Household Finances

Inflation’s impact on household finances is stark, as wages have failed to keep pace with rising prices, effectively reducing real income. For example, incomes in 2024-25 remain no higher than those in 2019-20 in certain regions despite inflation.

This erosion of purchasing power increases financial insecurity and contributes to rising food insecurity in affected populations. Families must stretch limited resources further, often facing difficult trade-offs.

The growing financial strain disrupts household stability, making it harder to save, invest, or plan for the future, thereby deepening economic challenges for many communities.

Financial and Mental Health Effects

The cost of living crisis causes a significant decline in purchasing power, leaving households unable to afford essential goods and services. Wages have stagnated, while prices rise continuously, increasing financial stress.

This financial pressure contributes to various mental health challenges, with many individuals experiencing anxiety and depression as they struggle to cope with the persistent economic demands.

Food insecurity and income stagnation further exacerbate the crisis, leaving vulnerable populations at greater risk and highlighting the urgency of addressing both financial and psychological impacts.

Decline in Purchasing Power

As inflation outpaces wage increases, real income effectively falls, reducing the ability of families to buy necessary items. This erosion of purchasing power means budgets are tighter than ever despite similar nominal earnings.

With essential costs such as food, rent, and utilities rising sharply, many households prioritize immediate needs, often sacrificing savings and discretionary spending to stay afloat.

The persistent gap between expenses and income contributes to a cycle of financial vulnerability, making long-term economic recovery difficult for affected families.

Psychological Impact of Financial Stress

Financial strain from the cost of living crisis manifests in increased anxiety, depression, and stress, impacting mental well-being. The constant worry about meeting basic needs takes a heavy psychological toll.

This stress can lead to sleep disturbances and impaired social relationships, further reducing quality of life and hindering people’s ability to effectively manage their finances.

Recognizing and addressing these mental health challenges is essential, with positive coping strategies and professional support playing important roles in resilience.

Understanding the Mental Toll

Research shows that prolonged financial hardship correlates strongly with poor mental health outcomes, emphasizing the need for accessible mental health resources during economic crises.

Food Insecurity and Income Stagnation

Income stagnation amid rising food prices leads to increased food insecurity, where families struggle to obtain enough nutritious food. This issue is a direct consequence of the mismatch between income growth and inflation.

Many households face difficult choices, balancing limited resources between essential bills and adequate food, which worsens health and social outcomes, particularly for children and vulnerable adults.

This alarming trend highlights the need for policy interventions and community support systems to help mitigate the growing hardship faced by many during the cost of living crisis.

Strategies for Personal Financial Resilience

Building financial resilience is crucial for navigating the cost of living crisis. Individuals must adopt practical strategies to manage incomes and expenses effectively despite rising costs.

By focusing on budgeting, expense control, and positive mental health practices, people can improve their ability to cope with economic challenges and reduce stress related to financial insecurity.

Budgeting and Managing Expenses

Creating a detailed budget allows individuals to track income and expenses, helping prioritize essential spending while reducing discretionary costs. This promotes better control over finances.

Setting realistic spending limits and focusing on needs rather than wants ensure that limited resources stretch further, preserving stability during periods of inflation and wage stagnation.

Regularly reviewing and adjusting budgets in response to changing expenses can empower households to adapt quickly to economic pressures and avoid unnecessary debt accumulation.

Positive Coping Mechanisms

Financial stress can impact mental health, so adopting positive coping strategies such as exercise, mindfulness, and social connection enhances emotional resilience during tough times.

Engaging in healthy activities helps reduce anxiety and depression linked to financial worries while fostering a mindset oriented toward problem-solving and self-care.

Seeking support from community groups or professionals when overwhelmed is vital for maintaining mental well-being alongside financial stability, enabling a holistic approach to resilience.

Business Approaches to Cost Challenges

Businesses face significant pressure due to rising operational costs amid the cost of living crisis. Adapting strategies to reduce expenses and protect profit margins is essential for sustainability.

This section explores practical approaches companies use to manage cost challenges while maintaining financial health and competitiveness in a constrained consumer market.

Implementing efficient cost controls and exploring revenue protection methods are critical for businesses to navigate economic uncertainty and ongoing inflationary pressures.

Reducing Operational Costs

To cope with higher expenses, businesses focus on reducing operational costs by renegotiating supplier contracts to secure better rates and more favorable terms. This helps lower input expenses significantly.

Adopting energy-efficient technologies and streamlining workflows also drive cost savings by improving productivity and minimizing waste, contributing to long-term financial benefits.

Companies increasingly invest in process automation and digital tools to enhance operational efficiency, reducing labor costs and error rates while maintaining quality standards.

Such cost control measures are vital in preserving liquidity and enabling businesses to withstand fluctuations in consumer demand triggered by the cost of living crisis.

Protecting Revenue and Profit Margins

Maintaining revenue amid declining consumer spending on non-essential goods is a major challenge. Businesses respond by diversifying product lines and focusing on essential or value-oriented offerings.

Dynamic pricing strategies and targeted promotions help protect profit margins, allowing companies to balance cost recovery with customer affordability.

Investing in customer loyalty programs and enhancing service quality strengthens relationships, encouraging repeat business even during economic hardships.

Overall, these revenue protection strategies enable businesses to sustain profitability while adapting to reduced consumer purchasing power and increased operational costs.